Okama Mcp

- 4 repo stars

- Updated June 22, 2026

- mbk-dev/okama-mcp

io.github.mbk-dev/okama-mcp is an MCP server that exposes okama portfolio analytics—backtests, Monte Carlo, efficient frontier, and PNG charts—to coding agents.

About

io.github.mbk-dev/okama-mcp is a Model Context Protocol server that wraps the okama Python library so AI coding agents can perform portfolio analytics on demand. developers shipping SaaS dashboards, internal tools, or research prototypes can ask an agent to backtest strategies, run Monte Carlo paths, plot efficient frontiers, and return PNG charts without manually scripting notebooks each time. Install via uvx from PyPI (runtimeHint uvx, version 1.4.0) and connect over stdio in Claude Code, Cursor, Codex, or other MCP-capable clients. It suits developers who already think in portfolios and want repeatable quant workflows inside agent sessions; it is not a brokerage, compliance layer, or live trading connector. Pair it with your own data ingestion and UI—the server focuses on analytics primitives the agent can chain into larger validate-or-grow workflows.

- Backtests and Monte Carlo via the okama library exposed as MCP tools

- Efficient frontier computation for allocation comparisons

- PNG chart generation for agent-readable visual outputs

- PyPI package okama-mcp v1.4.0 with uvx stdio transport

- MCP integration for Claude Code and Cursor—not a standalone trading app

Okama Mcp by the numbers

- Data as of Jul 27, 2026 (Skillselion catalog sync)

claude mcp add okama-mcp -- uvx okama-mcpAdd your badge

Show developers this MCP server is listed on Skillselion. Paste this into your README.

| repo stars | ★ 4 |

|---|---|

| Package | okama-mcp |

| Transport | STDIO |

| Auth | None |

| Last updated | June 22, 2026 |

| Repository | mbk-dev/okama-mcp ↗ |

What it does

Let your coding agent run portfolio backtests, Monte Carlo simulations, and efficient-frontier analysis with chart PNGs while you build fintech or personal-finance features.

Who is it for?

Best when you're prototyping fintech analytics, writing investment content, or validating allocation ideas with agent-driven quant steps.

Skip if: Skip if you need licensed investment advice, live execution, or enterprise portfolio management without Python/uvx setup.

What you get

After you register the server, your agent can request standardized analytics and chart outputs you can paste into docs, decks, or product prototypes.

- Backtest and Monte Carlo results from agent-invoked tools

- Efficient frontier analysis outputs

- PNG chart files suitable for docs or UI mocks

By the numbers

- Server version 1.4.0 on PyPI package okama-mcp

- Stdio transport with runtimeHint uvx

- Capabilities: backtests, Monte Carlo, efficient frontier, PNG charts per server description

README.md

okama-mcp

![]()

![]()

MCP (Model Context Protocol) server that exposes the okama investment portfolio toolkit to AI assistants — Claude Desktop, Claude Code, Cursor, Codex, and any other MCP-compatible client.

With okama-mcp installed, you can ask an AI things like:

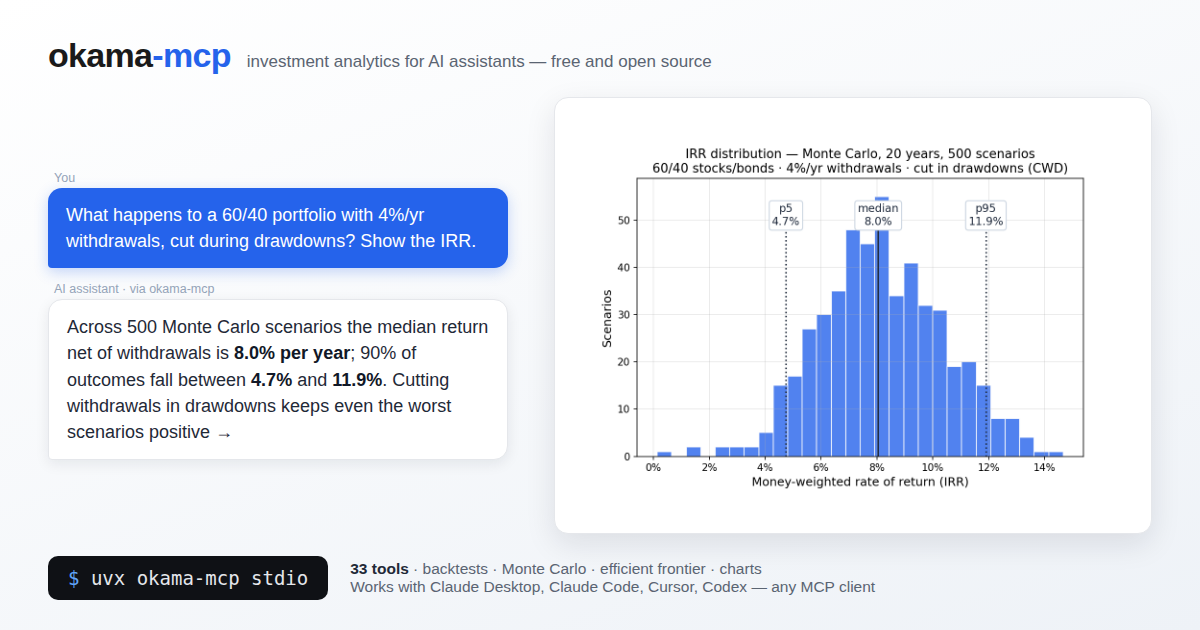

"Backtest a portfolio of 30% gold and 70% real estate over the last 15 years."

"Run a Monte Carlo retirement forecast on that portfolio, withdrawing $1,000/month indexed to inflation, over 25 years."

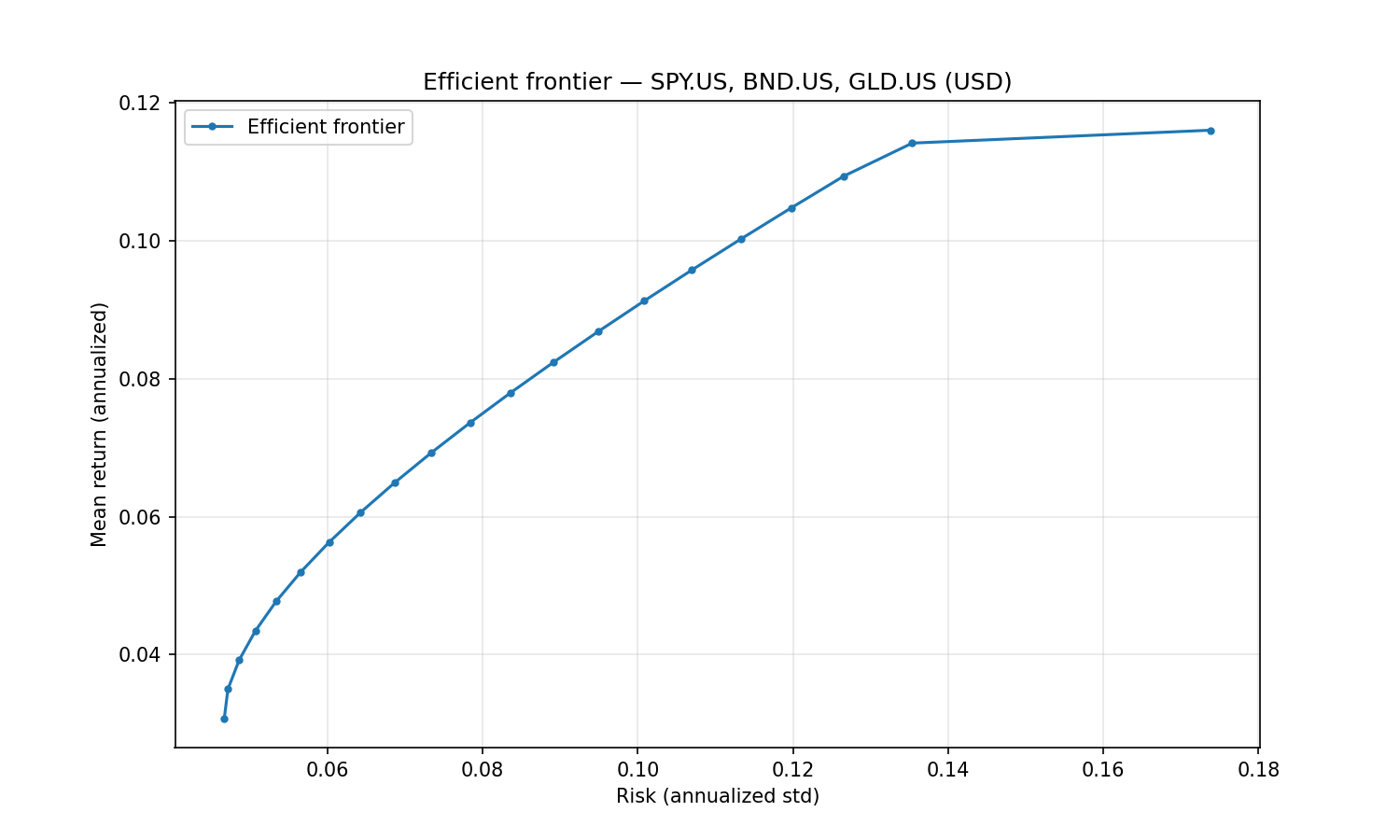

"What's the tangency portfolio of SPY, BND, and GLD with a 3% risk-free rate?"

…and the AI uses the MCP tools to call okama directly — no Python code needed.

Built on FastMCP. Single codebase, two transports:

stdio (for local clients) and streamable-http (for self-hosting).

okama-mcp is free and open source — no hosted service, no registration; you run it

yourself, locally or on your own server.

Install

Requires Python ≥ 3.11 (same floor as okama itself); okama ≥ 2.2.0 is installed automatically.

The easiest way — no clone, no venv — is uv or pipx:

uvx okama-mcp stdio # run straight from PyPI

# or

pipx install okama-mcp

Plain pip works too:

pip install okama-mcp

[!WARNING] With pip, prefer a dedicated virtual environment: on most modern Linux distros the system Python is marked externally managed (PEP 668), so

pip installoutside a venv fails, and a shared environment risks dependency conflicts. In your MCP client config, pointcommandat the absolute path of theokama-mcpscript inside the venv — GUI clients don't see your shellPATH.uvxandpipxavoid all of this by isolating the install automatically.

To work on the code, install from source instead:

git clone https://github.com/mbk-dev/okama-mcp

cd okama-mcp

poetry install

Run

# stdio — for Claude Desktop, Claude Code, Cursor (local IPC)

okama-mcp stdio

# streamable HTTP — for self-hosting on your own server

okama-mcp http --host 127.0.0.1 --port 8765

When running from a source checkout, prefix each command with poetry run.

Connect a client

Claude Desktop

Edit ~/Library/Application Support/Claude/claude_desktop_config.json (macOS) or

%APPDATA%\Claude\claude_desktop_config.json (Windows):

{

"mcpServers": {

"okama": {

"command": "uvx",

"args": ["okama-mcp", "stdio"]

}

}

}

Restart Claude Desktop; the server appears in the tools menu.

Claude Code

To make the server available in every project (works from any directory):

claude mcp add --scope user okama -- uvx okama-mcp stdio

Developers running from a source checkout can use claude mcp add okama -- poetry run okama-mcp stdio from the project root instead.

Or commit a .mcp.json at the project root so the whole team picks it up:

{

"mcpServers": {

"okama": {

"command": "uvx",

"args": ["okama-mcp", "stdio"]

}

}

}

Cursor

Add the server to .cursor/mcp.json in your project (or ~/.cursor/mcp.json to make

it global):

{

"mcpServers": {

"okama": {

"command": "uvx",

"args": ["okama-mcp", "stdio"]

}

}

}

Codex (CLI & Desktop)

Add the server with one command:

codex mcp add okama -- uvx okama-mcp stdio

Or declare it in ~/.codex/config.toml (or a project-scoped .codex/config.toml

in trusted projects):

[mcp_servers.okama]

command = "uvx"

args = ["okama-mcp", "stdio"]

The Codex CLI, desktop app, and IDE extension share this configuration — set it up once and it works in all three.

Self-hosting (streamable HTTP)

Run okama-mcp on your own server and share it across your MCP clients:

okama-mcp http --host 127.0.0.1 --port 8765 --path /mcp

(From source: poetry run okama-mcp http ...)

Then point your MCP client at http://<your-server>:8765/mcp. For a production

setup put nginx + TLS in front; ready-made examples live in deploy/:

deploy/systemd/okama-mcp.service— systemd unit (hardened, runs as a dedicated user)deploy/nginx/self-hosted.conf— nginx vhost: TLS, SSE-friendly proxying of/mcp

The server is open by design — free to run, no registration. If your instance must not be public, restrict access at the nginx level (allow-list, VPN, or HTTP basic auth).

Tool catalog

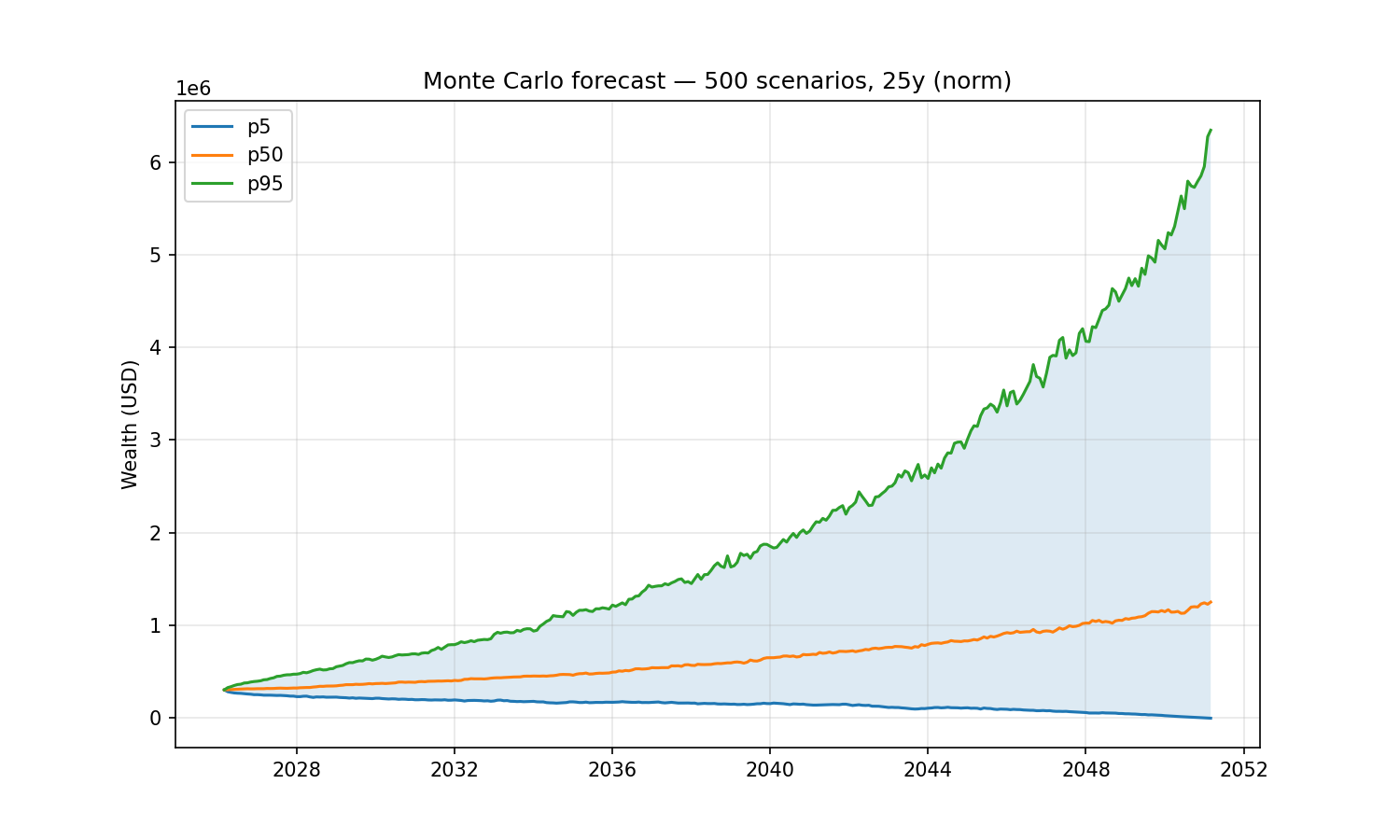

A Monte Carlo retirement forecast (30% gold / 70% real estate, withdrawing $1,000/month indexed to inflation over 25 years) and the efficient frontier of SPY/BND/GLD — the exact examples from the top of this page:

All tools are stateless — pass the full portfolio specification with every call.

The server caches expensive okama objects (Portfolio, EfficientFrontier) by content

hash, so repeated calls on the same spec are fast.

Nested portfolios. Wherever a list of assets is accepted — the assets field of

PortfolioSpec/FrontierSpec, or the portfolios argument on the comparison tools —

an entry may be a ticker string or a nested portfolio object (the same spec shape).

This lets you treat a whole portfolio as a single component: e.g. compare a 60/40

portfolio against gold, or put a sub-portfolio on the efficient frontier.

Search & metadata

| Tool | Purpose |

|---|---|

search_assets(query, namespace?) |

Free-text search across all okama symbols by name / ticker / ISIN. |

list_namespaces(kind="all"|"assets"|"macro") |

Show the available okama namespaces. |

get_asset_info(symbol) |

Metadata for one symbol — name, country, currency, type, date range. |

Single asset & comparisons

| Tool | Purpose |

|---|---|

get_asset_history(symbol, kind, first_date?, last_date?) |

Time series for one asset. kind ∈ {close_monthly, close_daily, adj_close, ror, dividends}. |

compare_assets(symbols, ccy, ..., portfolios?, rf_return?, t_return?) |

Side-by-side statistics (describe() table: CAGR, risk, drawdowns by period) plus Sharpe & Sortino per asset. |

get_correlations(symbols, ccy, ..., portfolios?) |

Correlation matrix of monthly returns. |

get_rolling_risk(symbols, ccy, window_months=12, ..., portfolios?) |

Rolling annualized risk per asset. |

get_asset_returns(symbols, ccy, ..., portfolios?, period?, real=False) |

Return metrics per asset: CAGR, cumulative return, mean / real mean return, monthly geometric mean, annual returns table. |

get_rolling_returns(symbols, ccy, window_months=12, real=False, ..., portfolios?) |

Rolling CAGR and rolling cumulative return per asset. |

get_benchmark_metrics(benchmark, symbols, ccy, ..., portfolios?, rolling_window?) |

Beta, correlation, annualized tracking difference and tracking error of each asset vs a benchmark/index. |

get_dividend_info(symbols, ccy, ...) |

LTM dividend yield, 5y mean yield, paying/growing streaks per asset. |

Portfolio backtest

| Tool | Purpose |

|---|---|

analyze_portfolio(portfolio, rf_return=0, t_return=0) |

Headline metrics (CAGR, annual mean/risk, Sharpe, Sortino) + full describe() for a PortfolioSpec. |

get_portfolio_drawdowns(portfolio) |

Drawdown time series + max drawdown / recovery period. |

get_portfolio_var_cvar(portfolio, time_frame=12, level=1) |

Historical Value at Risk and CVaR. |

get_portfolio_wealth_index(portfolio, full=False) |

Wealth-index series (cumulative growth of 1000). |

get_rolling_cagr(portfolio, window_months=12, real=False) |

Rolling CAGR time series (optionally inflation-adjusted). |

get_cagr_probability(portfolio, years, cagr_target) |

Historical probability of CAGR below a target (e.g. of a loss) over N-year periods. |

Monte Carlo DCF

| Tool | Purpose |

|---|---|

monte_carlo_forecast(portfolio, mc, cashflow) |

Forward simulation with one of five cash-flow strategies (indexation, percentage, time_series, vanguard, cut_if_drawdown). Returns percentile wealth bands, terminal-wealth stats, survival metrics. Includes the money-weighted IRR distribution (percentiles + mean). |

get_portfolio_irr(portfolio, cashflow) |

Historical money-weighted return (IRR) for a contribution/withdrawal plan. |

find_the_largest_withdrawals_size(portfolio, mc, cashflow, goal, ...) |

Largest sustainable withdrawal (Monte Carlo) for a goal: keep real purchasing power, keep nominal balance, or survive N years. |

get_monte_carlo_cash_flow(portfolio, mc, cashflow, discounting?) |

Monte Carlo distribution of future cash flows over time (percentile bands). |

The mc argument accepts distribution_parameters to override the fitted distribution (e.g. a fixed Student-t df); see the MCSpec shape below.

Distribution diagnostics

| Tool | Purpose |

|---|---|

get_distribution_fit(portfolio, mc) |

Goodness-of-fit for the return distribution: fitted parameters, Jarque-Bera, Kolmogorov-Smirnov (chosen + all distributions), and backtesting error (theoretical vs empirical mean/VaR/CVaR). |

get_return_moments(portfolio, mc, rolling_window?) |

Skewness & kurtosis time series — expanding, or rolling when a window (months) is given. |

optimize_students_df(portfolio, mc, var_level?) |

Degrees of freedom for a Student-t that best matches empirical VaR/CVaR. |

get_cagr_distribution(portfolio, mc, percentiles?, score?) |

Simulated CAGR at each percentile, plus the probability of a CAGR at/below score (e.g. score=0 → probability of a loss). |

DCF (historical cash-flow analysis)

| Tool | Purpose |

|---|---|

get_dcf_wealth_index(portfolio, cashflow, discounting?, include_negative_values?, discount_rate?) |

Historical wealth index with the cash-flow plan (FV nominal or PV discounted). |

get_dcf_cash_flow_ts(portfolio, cashflow, discounting?, remove_if_wealth_index_negative?, discount_rate?) |

Historical contribution/withdrawal time series (FV or PV). |

get_dcf_wealth_with_assets(portfolio, cashflow) |

Historical wealth index for the portfolio and each underlying asset. |

get_survival_period(portfolio, cashflow, threshold?, discount_rate?) |

Historical longevity: survival period (years) and depletion date. |

get_initial_investment_values(portfolio, cashflow, discount_rate?) |

Present value (PV) and future value (FV) of the initial investment. |

Efficient Frontier

| Tool | Purpose |

|---|---|

build_efficient_frontier(frontier) |

Full EF point table (Risk / Mean return / CAGR + per-asset weights). |

get_tangency_portfolio(frontier, rf_return, rate_of_return) |

Max-Sharpe portfolio on the EF. |

get_min_variance_portfolio(frontier) |

Global Minimum Variance portfolio. |

get_most_diversified_portfolio(frontier, target_return?) |

Most Diversified Portfolio (maximises the diversification ratio) on the EF. |

Macro

| Tool | Purpose |

|---|---|

get_inflation(currency, first_date?, last_date?, include_cumulative?, include_rolling?, include_describe?) |

Inflation series for a currency (USD, EUR, RUB, …). Optional: cumulative inflation, 12-month rolling inflation, describe() table. |

get_central_bank_rate(country, first_date?, last_date?, frequency="monthly"|"daily", include_describe?) |

Central-bank policy rate (US→US_EFFR, EU/ECB→EU_MRO, RUS→RUS_CBR, UK/GB→UK_BR, ISR→ISR_IR, CN/CHN→CHN_LPR1, or full symbol). Monthly or daily series; optional describe() table. |

get_indicator(symbol, first_date?, last_date?, include_describe?) |

Macro indicator from the RATIO namespace (e.g. USA_CAPE10.RATIO); bare country code defaults to that country's CAPE10. |

Charts

Each tool renders a PNG (default 1500×900) and returns it as MCP image content —

clients like Claude Desktop display it inline. Every chart tool also accepts

optional width / height (pixels, 300–4000) for custom sizes and aspect ratios,

and an optional save_path — the chart is then also written to that file and the

path reported back. Use save_path in clients that don't render MCP images in

their UI (e.g. Claude Code's terminal): ask for a chart "saved to /tmp/chart.png"

and open the file reference. Note: in self-hosted (streamable-http) deployments

save_path is written on the server's filesystem, not the client's machine.

| Tool | Chart |

|---|---|

plot_wealth_index(portfolio) |

Portfolio wealth index (+ inflation line). |

plot_drawdowns(portfolio) |

Drawdown depth over time. |

plot_monte_carlo(portfolio, mc, cashflow) |

Monte Carlo forecast fan (percentile bands). |

plot_irr_distribution(portfolio, mc, cashflow) |

Histogram of IRR across Monte Carlo scenarios (percentile markers). |

plot_qq(portfolio, mc) |

Q-Q plot of historical returns against the fitted distribution (norm/lognorm/t). |

plot_hist_fit(portfolio, mc, bins?) |

Histogram of historical returns with the fitted distribution PDF overlaid. |

plot_efficient_frontier(frontier) |

EF curve with individual asset points. |

plot_transition_map(frontier, x_axe="risk") |

Transition map: asset weights along the efficient frontier (x-axis = risk or CAGR). |

plot_assets(symbols, ccy, ..., portfolios?) |

Wealth-index comparison of individual assets. |

plot_macro(symbols, first_date?, last_date?, frequency="monthly"|"daily") |

Line chart of inflation / central-bank rate / CAPE10 series. Overlay multiple symbols (e.g. ["USA_CAPE10.RATIO", "EUR_CAPE10.RATIO"]). frequency='daily' valid only for .RATE symbols. |

Spec shapes

The complex tools take typed dicts validated by pydantic. The full schemas live in

src/okama_mcp/schemas.py; here are the headline shapes:

// PortfolioSpec

{

"assets": ["GLD.US", "VNQ.US"], // each entry: a ticker OR a nested PortfolioSpec

"weights": [0.3, 0.7], // optional, must sum to 1.0

"ccy": "USD",

"first_date": "2010-01",

"last_date": "2024-12",

"rebalancing_strategy": { // mirrors okama.Rebalance

"period": "year", // month | quarter | half-year | year | none

"abs_deviation": 0.05, // optional, |actual - target| threshold, 0 < x <= 1

"rel_deviation": 0.1 // optional, |actual / target - 1| threshold, > 0

},

"inflation": true

}

// MCSpec

{

"distribution": "norm", // norm | lognorm | t

"period_years": 25,

"scenarios": 500, // ≥ 1, no upper limit

"percentiles": [5, 50, 95],

"random_seed": 42, // optional, for reproducibility

"distribution_parameters": null // optional; null = fit from history (MLE). Lengths: norm [mu, sigma]; lognorm/t [shape|df, loc, scale]. Any element null = fit that one (e.g. [4, null, null])

}

// CashflowSpec — discriminated by `type`

{ "type": "indexation", "initial_investment": 1000000, "frequency": "month", "amount": -1000, "indexation": "inflation" }

{ "type": "percentage", "initial_investment": 1000000, "frequency": "year", "percentage": -0.04 }

{ "type": "time_series", "initial_investment": 100000, "events": { "2030-06": -50000 }, "time_series_discounted_values": false }

{ "type": "vanguard", "initial_investment": 1000000, "percentage": -0.04, "floor_ceiling": [-0.025, 0.05], "indexation": "inflation" }

{ "type": "cut_if_drawdown", "initial_investment": 1000000, "frequency": "year", "amount": -60000, "indexation": "inflation",

"crash_threshold_reduction": [[0.2, 0.4], [0.5, 1.0]] }

// FrontierSpec

{

"assets": ["SPY.US", "BND.US", "GLD.US"],

"ccy": "USD",

"bounds": [[0.0, 0.7], [0.1, 1.0], [0.0, 0.3]], // optional

"n_points": 20,

"rebalancing_strategy": { "period": "year" },

"inflation": false

}

// Nesting — a portfolio used as a single component (works in PortfolioSpec /

// FrontierSpec `assets`, and the `portfolios` argument of the comparison tools):

{

"assets": [

"GLD.US",

{ "assets": ["SPY.US", "AGG.US"], "weights": [0.6, 0.4], "symbol": "bench6040.PF" }

],

"weights": [0.3, 0.7] // one weight per top-level entry

}

Development

The project follows TDD (see AGENTS.md). After every code change run:

poetry run pytest -q

poetry run ruff check .

To run the live-API integration test (hits api.okama.io):

poetry run pytest -m integration

Project layout

src/okama_mcp/

├── server.py # FastMCP instance + registration entry point

├── transport.py # CLI: `okama-mcp stdio | http`

├── schemas.py # PortfolioSpec, MCSpec, CashflowSpec, FrontierSpec

├── cache.py # TTL+LRU cache keyed by sha256 of canonical spec

├── serialization.py # pandas → JSON-safe with smart truncation

├── errors.py # Translate okama exceptions to actionable MCP errors

└── tools/

├── search.py, asset.py, asset_list.py

├── portfolio.py, monte_carlo.py

├── frontier.py, macro.py

└── plots.py

License

MIT — same license as okama itself.

Recommended MCP Servers

How it compares

MCP quant toolkit backed by okama, not a hosted robo-advisor or spreadsheet add-in.

FAQ

Who is io.github.mbk-dev/okama-mcp for?

Developers and small teams who use Claude Code or Cursor and want portfolio backtests, Monte Carlo, and efficient-frontier charts through MCP tools.

When should I use io.github.mbk-dev/okama-mcp?

Use it during grow-phase analytics or validate-phase pricing scenarios when you need repeatable portfolio metrics and PNG visuals inside an agent session.

How do I add io.github.mbk-dev/okama-mcp to my agent?

Add the PyPI package okama-mcp (v1.4.0) with uvx stdio transport to your MCP config per the server schema, then restart the client.